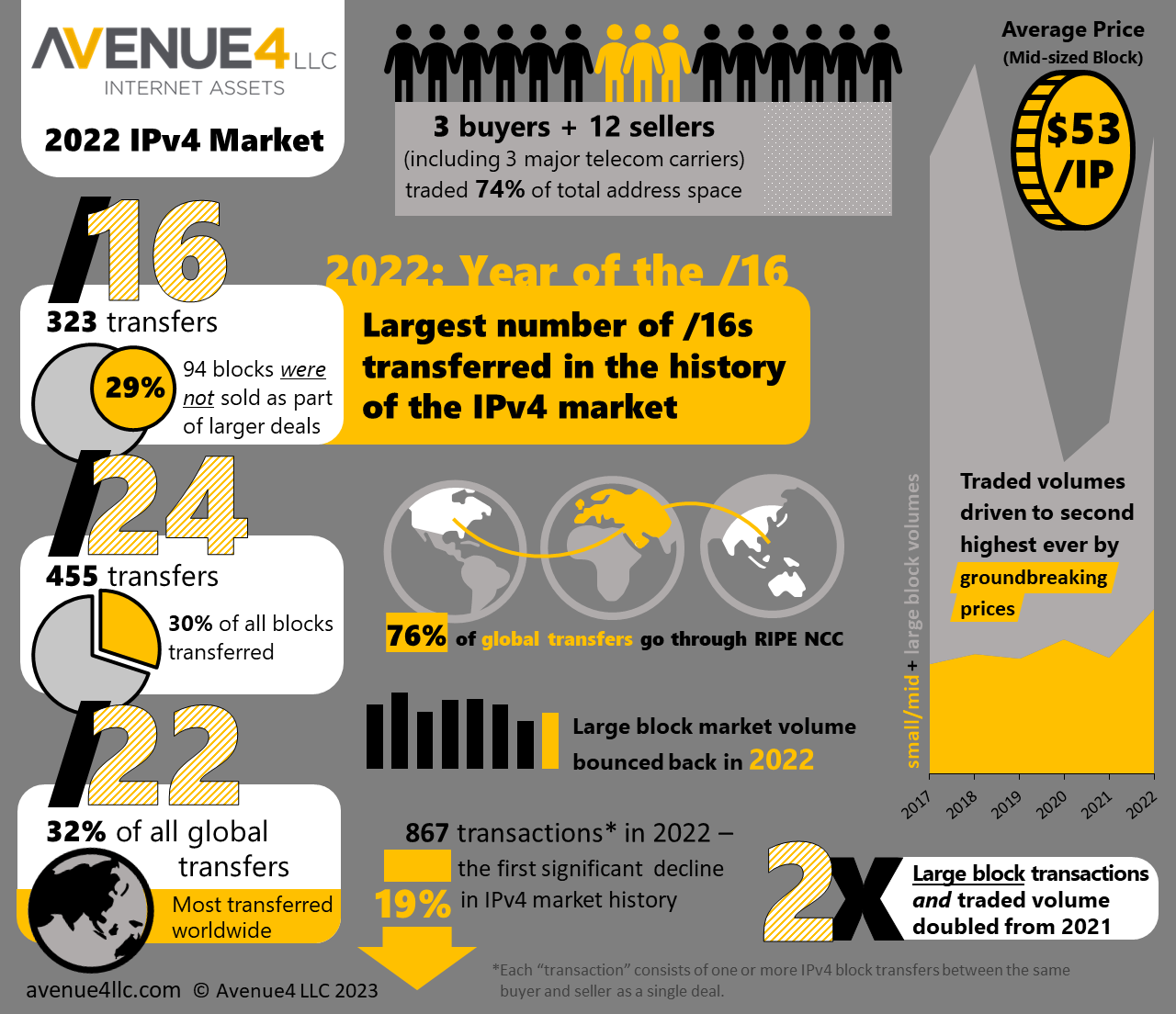

In 2021, the story was price. In 2022, the story was price and large block supply. Spurred by unprecedented unit pricing, the IPv4 market in North America experienced its second-best year ever in market history.

Nearly double the number of IPv4 addresses were traded in 2022 compared to 2021, predominantly due to the increased flow of large block supply from twelve sellers, five of whom were first-time market participants.

2022 was a year of many firsts:

InterRIR transactions, which have averaged less than 13% of total traded volume since 2015, peaked at 25%

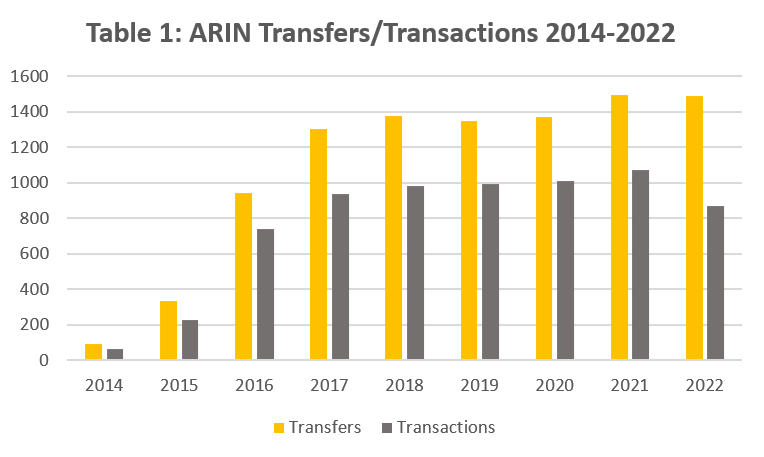

Despite these many firsts in 2022 -- all strong positive market indicators -- the market experienced its first material declining indicator. The number of transactions dipped by nearly 20%. (See Table 1).

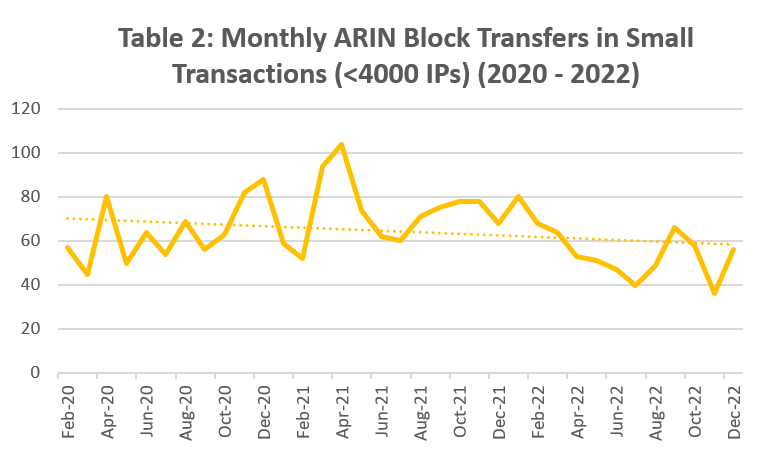

Historically, transfers and transactions have followed similar trajectories. In 2022, however, their paths diverged, principally due to a gradual decline in small block transfers and transactions over the last two years (see Table 2). Small block pricing also declined in the last half of 2022.

These shifts in the small block market alone are not yet signaling weakness in the IPv4 market, particularly given that the total volume of numbers traded reached its second highest level in history. This small block decline is more likely pointing to cyclical trends in this sector of market. Exceptional price points generated the most robust large and mid-size block markets to date, and the small block market may yet resume its upward trajectory. Only time will tell.

This is what we do know heading into 2023: We appear a long way from any precipitous decrease in IPv4 market activity. Overall market demand for IPv4 space is still strong. Supply is still not keeping pace with demand but rapid price increases in the last year are likely to result in some pull back by buyers or other efforts to relieve some of the upward pricing pressures. Meanwhile, there is little evidence that buyers and sellers are driving IPv6 adoption.

This infographic presents the essential information for IPv4 market participants. We hope you will find it useful in evaluating the challenges and opportunities in the coming year.